Back on Track

Market attention remained fixated on developments in the Middle East.

The announcement of a temporary ceasefire early in April boosted market confidence, with asset prices recovering. Investor enthusiasm cooled somewhat towards the month-end, as it became apparent that a permanent resolution was no certainty in the near-term.

At the time of writing, the Strait of Hormuz - the shipping channel bordering Iran that supports around 20% of global oil and gas supply - remains effectively shut.

Key Points:

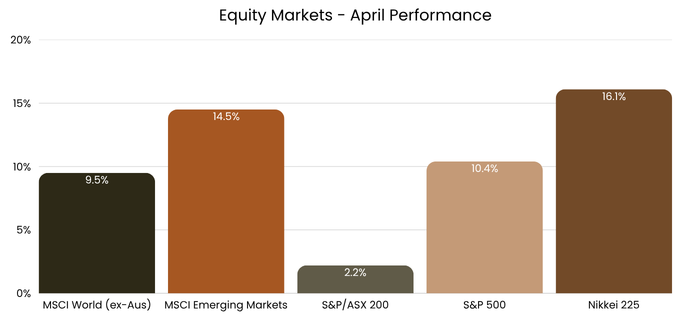

Markets rebound to recover losses from March, with major equity indices positive in 2026

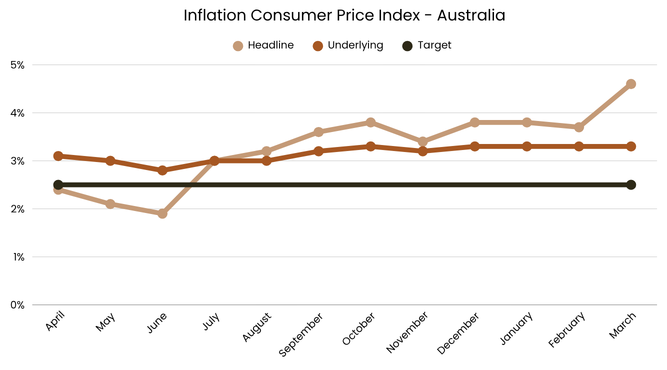

Headline inflation in Australia hit 4.6%, with underlying inflation at 3.3%

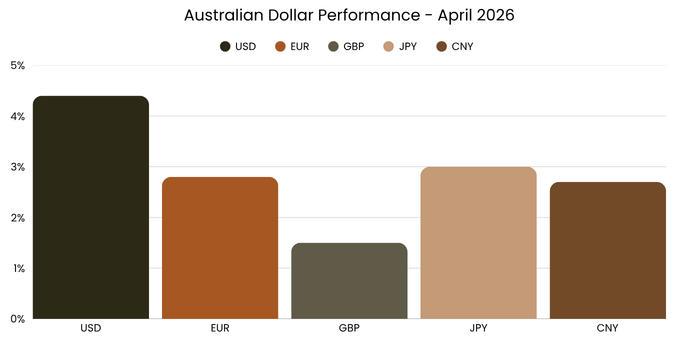

Australia Dollar hits $0.72 against the US dollar, its highest point since 2022

However, the ongoing dialogue between the United States and Iran suggests both sides do not want a prolonged conflict.

The larger issue is when that resolution will be agreed upon. Economies, including Australia, are grappling with higher energy and petrol costs, which appear to be permeating into other sectors such as construction, manufacturing and consumer goods. A prolonged conflict also risks entrenching inflation.

On a positive note, markets have largely recovered losses from March. The MSCI World Index (ex-Australia), for example, is up 5.6% year-to-date. Closer to home, the ASX/200 has squeezed out a modest 0.54% gain.

The overriding message for investors is that when volatility hits, it’s important to stick with your strategy. It’s easy and even understandable to become emotional when asset prices fall, but it’s equally important to zoom out and remember the power of compounding over years, not weeks or months.

Periods of volatility are an inevitable part of investing, and part of our role as your advisor is to help guide you through them. Should you wish to discuss recent market developments or your portfolio in more detail, please reach out to your advisor.

Please click here to read our April 2026 markets report as a PDF.

Australian Economy

Headline inflation reached 4.6% in March as the Iran war continued to choke global supply chains. Underlying inflation remained steady at 3.3%, structurally above the RBA’s 2.5% target.

The largest contributors to annual inflation were housing (+6.5%), transport (+8.9%) and food and non-alcoholic beverages (+3.1%), highlighting the growing strains households are facing.

Goods inflation reached 5.5%, up from 3.5% in February. Automotive fuel was the main culprit, rising 32.8%, representing the strongest monthly increase since the series began in 2017.

Data Source: Australian Bureau of Statistics

Business confidence recorded its second-largest monthly fall on record. Forward orders fell, while purchase cost growth more than doubled to 3%. Consumer sentiment fell 12.5% to 80 points. Expectations of family finances and economic conditions deteriorated meaningfully compared to March.

Unemployment remains resilient at 4.3% in March. However, job loss fears jumped to a 10-year high, excluding the COVID pandemic.

The Reserve Bank of Australia did not convene in April, with the next meeting scheduled for May 5. Markets have moved to price in a third rate hike for 2026, taking the cash rate to 4.1%.

Equities

Following the sharp declines in March, equity markets globally rallied in April. The MSCI World Index (ex-Australia) finished 9.5% higher supported by double-digit returns in Japan, Korea and the United States.

Data Source: Western Australia Treasury Corporation

Samsung and Taiwan Semiconductor roared higher on renewed optimism around artificial intelligence. In the US, the S&P 500 gained 10.5% in line with the gains to technology companies and robust corporate earnings. Apple announced long-time CEO Tim Cook would be succeeded by John Termus.

The ASX 200 gained 2.2% but underperformed other developed equity markets due to its lower weighting to technology stocks.

Fixed Income

Bond yields inched higher in April following the gains of March.

Australian Government 10-year bond yields increased 9 basis points to 5.06%, and are ~30 basis points higher than before the Iran war. That reflects both extra risk premium demand from a global conflict, in addition to expectations of higher interest rates.

Similarly bonds in Japan, the United Kingdom and Germany have also increased. The overall result is fixed income looking relatively more attractive to new investors seeking income.

Currencies

The Australian dollar outperformed major trade partners in April as markets adjusted domestic interest rate expectations.

Data Source: TCorp

While most central banks, including the US Federal Reserve, Bank of Japan and Bank of England, acknowledged inflation risks, none have moved to raise policy rates. Conversely, Australia has pushed through two rises in February and March, with another expected in May. That makes the Australian currency more attractive to traders, who can park cash in government deposits with higher yields than in other “safe” jurisdictions.

Against the US dollar, the Australian dollar increased 4.4% to $0.72, reaching its highest level since 2022.

Commodities

Commodities continued to march higher, gaining 4.2% in April. Oil remained the epicentre of market attention, with prices gyrating wildly in response to developments between the United States and Iran. At one point, the price reached USD$126 per barrel, before finishing the month closer to USD$114. This compares to the pre-conflict price hovering around US$70.

Overall, the Bloomberg Commodity Index has gained 30% in 2026, led by a 74% increase in the energy sector. Gains in crude oil, diesel and gasoline have broadened to adjacent commodities such as fertilisers, copper and wheat. What was once an oil shock appears to be evolving into a broader commodity inflation cycle.

General Advice Disclaimer: The information and opinions within this document are of a general nature only and do not consider the particular needs or individual circumstances of investors. The Material does not constitute any investment recommendation or advice, nor does it constitute legal or taxation advice. Zuppe International Pty Ltd (ABN 12 628 405 952)

(The Licensee) does not give any warranty, whether express or implied, as to the accuracy, reliability or otherwise of the information and opinions contained herein and to the maximum extent permissible by law, accepts no liability in contract, tort (including negligence) or otherwise for any loss or damages suffered as a result of reliance on such information or opinions.

The Licensee does not endorse any third parties that may have provided information included in the Material. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Therefore, any stated figures should not be relied upon. The investment return and principal value of an investment will fluctuate so that an investor’s investments, when redeemed, may be worth more or less than their original cost.