Middle East Ruptions

For much of February, market attention was on artificial intelligence. In recent years, technology companies and more broadly markets have rallied strongly, supported by growing demand for computing power and the rapid development of AI models such as ChatGPT.

However the narrative shifted as markets began to discern the potential losers, particularly software companies where their business models may face disruption.

Key Points:

Oil prices surge, equities fall as the US, Israel initiate military action against Iran

The Reserve Bank of Australia raised the cash rate by 25 basis to 3.85%

Technology and software companies retreat as investors increasingly price in the risk of AI disruption.

Toward the end of the month, geopolitical developments began to dominate market sentiment. On February 28, the US, alongside Israel, launched a military offensive against Iran with the ultimate goal of regime change.

In early March, both equity and bond markets meaningfully retreated. Financial markets rarely respond well to uncertainty, and an open-ended military conflict with no clear resolution introduces precisely the kind of uncertainty investors tend to avoid.

It is important to remember, however, that geopolitical conflicts have historically influenced financial markets. While uncomfortable, market turbulence is inevitable and often temporary.

Lawrance Private Wealth maintains a long-term approach to investing. We take confidence in our diversified and disciplined approach to portfolio construction, whereby we mitigate risk across geographies, asset classes and security selection.

Our Investment Committee continues to actively monitor markets and regularly review portfolio positioning.

If you have any questions or concerns, please do not hesitate to reach out to your adviser.

Please click here to read our February 2026 markets report as a PDF.

Australian Economy

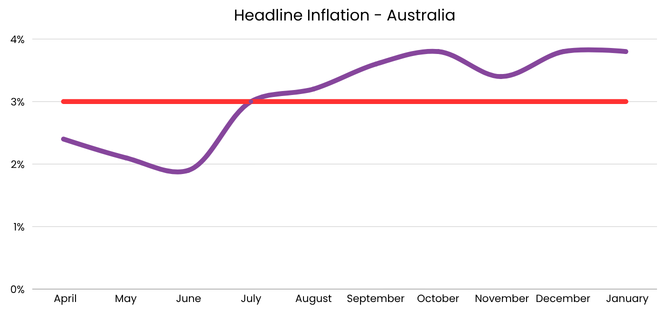

The Reserve Bank of Australia increased the cash rate by 25 basis points to 3.85% in February, following several months of elevated inflation data.

Inflation figures released later in the month showed headline inflation rising to 3.8%, while underlying inflation reached 3.4%. This marked the sixth consecutive month that underlying inflation has remained above the Reserve Bank’s target range of 2–3%.

Data Source: Australian Bureau of Statistics

Meanwhile, the unemployment rate remained steady at 4.1%, highlighting continued tightness in the labour market.

Wage growth increased by 0.8% over the quarter, bringing annual wage growth to 3.4%.

While this is a welcome development, wages are still rising more slowly than inflation. As a result, real wages remain negative, meaning the cost of living is increasing faster than incomes.

Persistently negative real wages reduce purchasing power and can ultimately weigh on household consumption.

Looking ahead, attention will turn to the May Federal Budget and how the government plans to address ongoing cost-of-living pressures.

As discussed in our January outlook, addressing these challenges will likely require structural policy responses to ease supply constraints across the economy.

Equities

The ASX 200 closed the month 4.1% higher, supported by strong performance in the financials and materials sectors. The major banks released earnings updates that were broadly well-received by investors and were further supported by the prospect of higher interest rates.

Global equities recorded a modest gain of 0.5% for the month. Performance was weighed down by the US market, where the S&P 500 declined 0.9% largely due to its heavy exposure to technology companies.

Investors soured on technology names as focus shifted from the potential winners of artificial intelligence to those that could face disruption. Software companies were particularly affected, with investors reassessing how AI could impact existing business models. Some firms have already begun adjusting to these changes. For example, Atlassian announced a reduction of around 10% of its workforce.

Elsewhere, equity markets performed strongly. The FTSE 100 rose 6.7%, while the MSCI Emerging Markets Index gained 5.6%. Japan was the standout performer, with equities rallying 10.4% following the election of the pro-growth Liberal Democratic Party.

Fixed Income

After increasing in January, global bond yields eased. Ten-year government bond yields in the United States, Germany and Japan fell by 30 basis points, 20 basis points and 13 basis points, respectively.

Australian bond yields also moderated, declining 16 basis points to 4.65%. This follows a sharp rise over the past three months, as markets have increasingly priced in the possibility of further interest rate hikes by the RBA.

Currencies

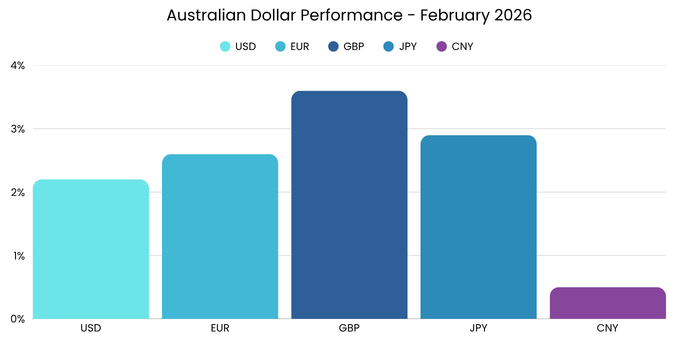

The Australian dollar delivered another strong month, with the trade-weighted index reaching its highest level in over eight years. Persistent domestic inflation and resilient employment have reinforced expectations that Australian interest rates will remain relatively elevated, increasing the currency’s attractiveness to yield-seeking investors.

All else being equal, a currency will typically increase in value against peers when interest rates are expected to rise.

Against the US Dollar, our local currency surpassed $0.71, its highest point since 2022. The AUD also recorded strong gains against the Pound and Japanese Yen.

Data Source: Western Australia Treasury Corporation

Commodities

Amid conflict in the Middle East, oil shot higher. Brent crude increased 2.5% to US$72.50 in February, before exceeding $97/barrel in the early days of March. Markets increasingly factored in the risk of a closure of the Strait of Hormuz: a vital shipping passage responsible for about 20% of global oil trade.

In contrast, several industrial commodities declined. Prices for resources such as iron ore, copper and nickel eased as expectations for slower global economic activity weighed on demand. Gold, meanwhile, continued its upward trajectory as investors sought risk-off assets.

General Advice Disclaimer: The information and opinions within this document are of a general nature only and do not consider the particular needs or individual circumstances of investors. The Material does not constitute any investment recommendation or advice, nor does it constitute legal or taxation advice. Zuppe International Pty Ltd (ABN 12 628 405 952)

(The Licensee) does not give any warranty, whether express or implied, as to the accuracy, reliability or otherwise of the information and opinions contained herein and to the maximum extent permissible by law, accepts no liability in contract, tort (including negligence) or otherwise for any loss or damages suffered as a result of reliance on such information or opinions.

The Licensee does not endorse any third parties that may have provided information included in the Material. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Therefore, any stated figures should not be relied upon. The investment return and principal value of an investment will fluctuate so that an investor’s investments, when redeemed, may be worth more or less than their original cost.